Shaking Up the Market

It’s May 2025, and I’m in Las Vegas. My colleagues and I order burgers and fries from the restaurant touchscreen. Instead of whipping out my card, I pay via a QR code. One snap, and the order completes. Five minutes later, we’re sitting at our table, chowing down on steak burgers and tallow-cooked fries — better than most of the food you’ll find on The Strip.

The store made a higher profit margin on the burgers, but we didn’t pay a single cent more. How is this possible?

This particular burger joint is not a family-run, single-location roadside diner, but it used to be. Steak ‘n Shake used to grind meat in front of customers to show the quality of their burgers. Their first restaurant opened in Normal, Illinois, in 1934. Nearly one hundred years later, the chain boasts over 400 restaurants. The story of every business that scaled from SMB to global brand starts in the same place — the mom and pop shop, rooted in the founder’s values of honesty and value for money. While I eat my burger, I think about why some fast food restaurants scale, and others struggle. Against the backdrop of shrinking profits for other conglomerates like McDonald’s and Burger King, this burger business is booming.

During May 2025, Steak ‘n Shake hit the headlines as they presented the results of one simple change to their business. A few months earlier, they started to accept Bitcoin payments.

In this article, we’ll look at the sales figures and numbers of Steak ‘n Shake post Bitcoin adoption. I’ll outline how they went about implementing their strategy, and I’ll share the types of businesses that can benefit the most from following suit.

Before we get there, let’s take a step back and consider the current situation with Point of Sale (PoS) payment processors and how SMBs charge customers.

Card Payments: A Raw Deal for SMBs

Margins are tight, especially for small businesses. A lot of people I know would roll their eyes at cafes and bodegas with a $10 minimum for cards. Cards are convenient. But, SMBs have every right to ask for cash for lower-value transactions because payment processing fees are astronomical. The Starbucks and Walmarts of this world might be able to swallow the typical 3-5% fees without any problem, but smaller merchants get a raw deal whenever customers use plastic instead of cash.

Consumers don’t care, but 3% additional profit and faster settlement could be a lifeline to a lot of businesses that accept a high number of low-value transactions.

Examples of high-volume low-ticket businesses:

- Barbers

- Food trucks

- Coffee shops

- Local newsstands

- Nail salons / beauty parlors

- Quick service restaurants

- Neighborhood laundromats

- Express exterior car washes

- Small ice cream / gelato shops

- Independent convenience stores / bodegas

- Used book stores (for low-priced paperbacks)

- Discount/dollar/thrift stores (Independent)

- Small farmers’ market produce stands

- Local stationery/school supply shops

- Tire shops / oil change stations.

- Small hardware stores

- Parking lots / garages

- Smoke shops

- Bakeries

In a recent article titled Moving Value Like Information, Roy Sheinfeld, CEO of Breez, explained why the current payment processing model is so expensive (and outdated).

“A fintech payment involves an indefinite chain of intermediaries. For each intermediary to earn revenue from the transaction, they need a billing model. And they opt for discrete payments because that is what regulated money transmitters are allowed to do. Thanks to the KYC, AML, and risk assessment involved, it’s an expensive business, so their fees are commensurately high.”

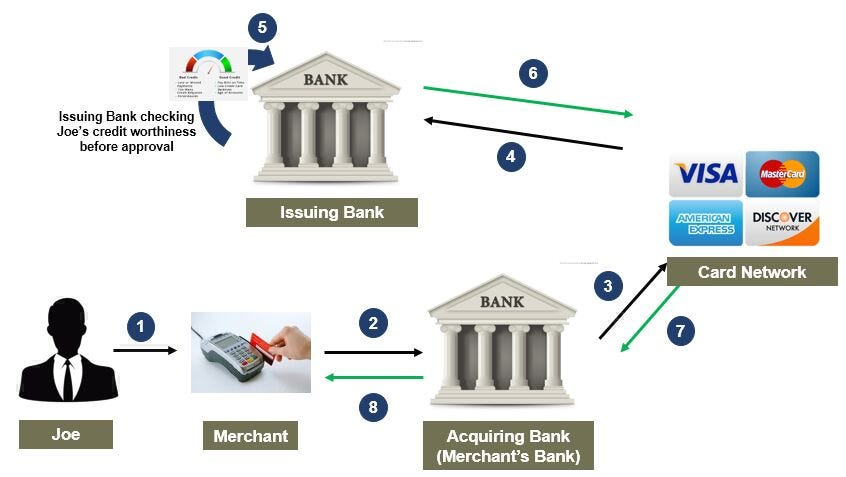

Card payments follow the ISO8583 protocol. The first version was created in 1987, with more recent versions being standardized in 1997 and 2003.

Since every network implements this protocol differently, an ISO8583 message on the Mastercard network differs from an ISO8583 message on the Visa network. This payment flow diagram and gives a general overview of how the purchase process works, but cannot address the specifics of each card network.

Authorization Stage:

This process, while complex, typically happens within seconds. But it’s important to note that no money has moved at this point.

In fact, card networks don’t ever receive or store our money; they only process information. Essentially, they are software companies. For that reason, they are not even regulated as banks or financial service providers are. Yet they earn a sizable commission on the thousands of transactions they facilitate every second.

In essence, the authorization stage checks if the transaction is valid. The settlement stage transfers the money. And it can take several days to actually receive the funds.

- Imagine earning 3% more profit on every transaction (or offering customers 3% better value).

- Imagine putting aside some of the savings as a cash reserve for your business.

- Imagine restocking when you need and paying suppliers sooner because of instant settlement.

- Imagine no headaches with chargebacks or failed payments.

There is one payment system that can help businesses in these ways, and it’s the same one I used to buy a hamburger and fries in Las Vegas. Accepting bitcoin payments radically changes things for high-volume, low-ticket businesses.

P2P Electronic Cash Offers Merchants A Better Deal

In the whitepaper published by Satoshi Nakamoto on October 31st, 2008, Bitcoin is described as ‘a peer-to-peer electronic cash system.’ Although it is now primarily used as a store of value in the West, its value lies in its utility as a permissionless, immutable, and publicly auditable medium of exchange. Nakamoto knew that for a digital token to be considered a commodity, an asset, or money, it must demonstrate utility first.

But wait, doesn’t Bitcoin take 10 minutes to complete one transaction? That doesn’t sound ideal for my business. No one wants to wait that long to make a purchase.

After 16 years of constant operation, many technological solutions have been implemented to make Bitcoin payments instant and virtually fee-free. For customers to want to use Bitcoin to pay, the interface must be as simple as tapping their credit card or phone. Remember, they are essentially willing to pay a 3% premium for this convenience.

The Lightning Network, launched in 2017, is a ‘Layer 2’ solution that allows instant transactions on Bitcoin. Primarily, it is used for lower amounts (e.g., less than $1,000), which makes it perfect for high-volume, low-ticket businesses. Think of it as passing digital bills straight to the merchant, rather than making a (slower) bank transfer on the base-layer blockchain. Importantly, bitcoin on Lightning is not IOUs. All funds can be self-custodied and put back ‘on chain’ (returned to the base layer) at any time.

By 2025, the Lightning ecosystem is thriving, with dozens of wallet apps available, integrations in major platforms like Shopify, Woo Commerce, and CashApp, 13,000 physical merchants accepting payments, 75,000 open payment channels, over 4,000 BTC of capacity, and the ability to process millions of payments per second.

How does a payment work?

It’s much simpler than the last graphic. The payment is routed directly from the customer’s wallet, through open payment channels, straight to the merchant’s wallet. No chargebacks, no waiting period, no third-party approval. Confirmation is typically faster than Visa or Mastercard.

Payments are usually made by snapping a QR code and hitting ‘pay’. At Steak ‘n Shake, the Lightning payment just worked. The QR code was frictionless, with no invoicing or issues. No customer support or training needed for the servers, either. Buying a hamburger using Lightning was easier than buying a bottle of water using an American Express chip card.

YouTube Video of Natalie Brunell using Bitcoin payments at Steak ‘n Shake to buy a burger: https://youtube.com/shorts/5Xhqkfrf_s8?si=5OKlZUIRQp4sl2qF

Steak ‘n Shake — A Case Study

After rolling out Bitcoin POS integration to their 400+ stores worldwide in May, Steak ‘n Shake has posted some mind-boggling results. While many smaller businesses have already added Lightning payments to their set-up, fewer bigger businesses have done so. Being an early mover in Bitcoin brings huge advantages.

Steak ‘n Shake was able to generate positive PR buzz and attract the support of the Bitcoin community by announcing Lightning integration. In fact, on launch day, one out of every 500 Bitcoin transactions globally happened at Stake ‘n Shake!

As COO Dan Edwards explained in his Bitcoin 2025 speech, same-store sales increased by over 10%, with even stronger results driven by the 50%+ savings in processing fees. None of this came at the expense of customers, as bitcoin payments prove faster than credit card transactions.

“All the benefits that we get from Bitcoin, whether it’s gaining in customer traffic and same store sales or whether it’s reducing our fees, allow us to reinvest in the quality of our products and also other very important initiatives such as removing seed oils from all of our restaurants.” Dan Edwards, COO, Steak ‘n Shake.

The ‘bitcoin bump’ was one factor in the company’s P&L transformation too — +$50.9 million net in Q2 2025, compared to -$48.2 million in Q1 2025.

The lesson I’ve seen with Steak ‘n Shake is to not ‘dip your toe’ or do a quiet soft launch. This is a brash, freedom-loving brand that harnesses the support of a passionate community by pushing back on liberal trends and companies that are terrified of offending customers.

Steak ‘n Shake spread the news about their rollout far and wide. They created a burger especially for bitcoiners to try, and they lean into ‘based’ food habits (e.g., no seed oils). Announced 10/31/2025 on Bitcoin White Paper Day (the 17th anniversary), the company announced even more support for the Bitcoin ethos and community. They will use all Bitcoin earned as a strategic reserve to help their balance sheet (as we discussed in my last column), and will donate a portion of earnings from their Bitcoin meal towards open source development. Finally, they have created a cross promotion with Fold App (a Bitcoin rewards credit card).

Not every brand has to put Bitcoin at the center of their marketing campaign, but it’s a good idea to feature it or at least slap a ‘Bitcoin accepted here’ sticker on the door. That’s how to attract additional customers and to gain the respect of this group of loyal customers.

Why Bitcoin Payments are a Win-Win

It’s rare that a new technology comes along without an owner looking to draw profits. Most of Bitcoin and Lightning’s development has been provided open-source (for free) by passionate advocates or facilitated by peer-to-peer electronic cash donations. The solutions that enable Lightning payments at Steak ‘n Shake make fractions of a cent on each transaction. They only win through wider adoption.

With so many rent-seeking tech-owners, Bitcoin payments are win-win for customers and merchants. This is the first digital payment technology you could say this about.

Customers now have a greater choice in how to pay. They can choose to spend dollars, or they can pay with self-custodied money, which helps businesses reduce prices or increase quality. Many bitcoiners want to support enterprises that align with their ideals. As we enter into an era of greater digital surveillance and control, the ideals of freedom will become increasingly more important.

For merchants, the benefits are obvious. Slashing costs to the business (lower payment-processing fees), attracting new customers, and generating local PR buzz. As Bitcoin payments become the standard, there really are no losers (apart from Visa, Mastercard and American Express).

Most importantly for the business owners reading this column, you have an even greater opportunity than the Steak ‘n Shake executives. Small and Medium-sized Businesses do not have a board of directors to educate. You do not have thousands of shareholders to please. You don’t have 50+ locations with huge numbers of staff to train. If you are willing to integrate Lightning payments, you can set it up tomorrow. As we say in Bitcoin, ‘You can just do things!’

The implementation costs are minimal, and there is a range of options, from Bitcoin PoS terminals, through self-custody wallets on your phone, to open-source software integrations with BTC Pay Server.

Announcement on X: https://x.com/realgoodcoffee1/status/1978550329248526685

One incredible development in the last month is the launch of Bitcoin payments on all Square PoS terminals. The full rollout to 4 million merchants using Square takes place on November 11th, so it’s likely that some business owners reading this will be able to accept Bitcoin payments without lifting a finger. Tax reporting, invoices, and all other paperwork are all ready at the touch of a button.

There are more than 4 million SMBs in America — 34 million in fact. This leads me to a couple of questions.

- What will the other 30 million merchants use to integrate Bitcoin Lightning payments?

- What kinds of support will these businesses need to help them manage self-custody, saving, offramping, and balance-sheet strategy?

However the space develops, Bitcoin is becoming a more widely accepted form of payment day by day. The advantages for business are clearer than ever before. Will you be a first mover, or will you let this opportunity pass you by?

If you have any questions, you can book a meeting by reaching out to Jeff at jeff@sovreign.io